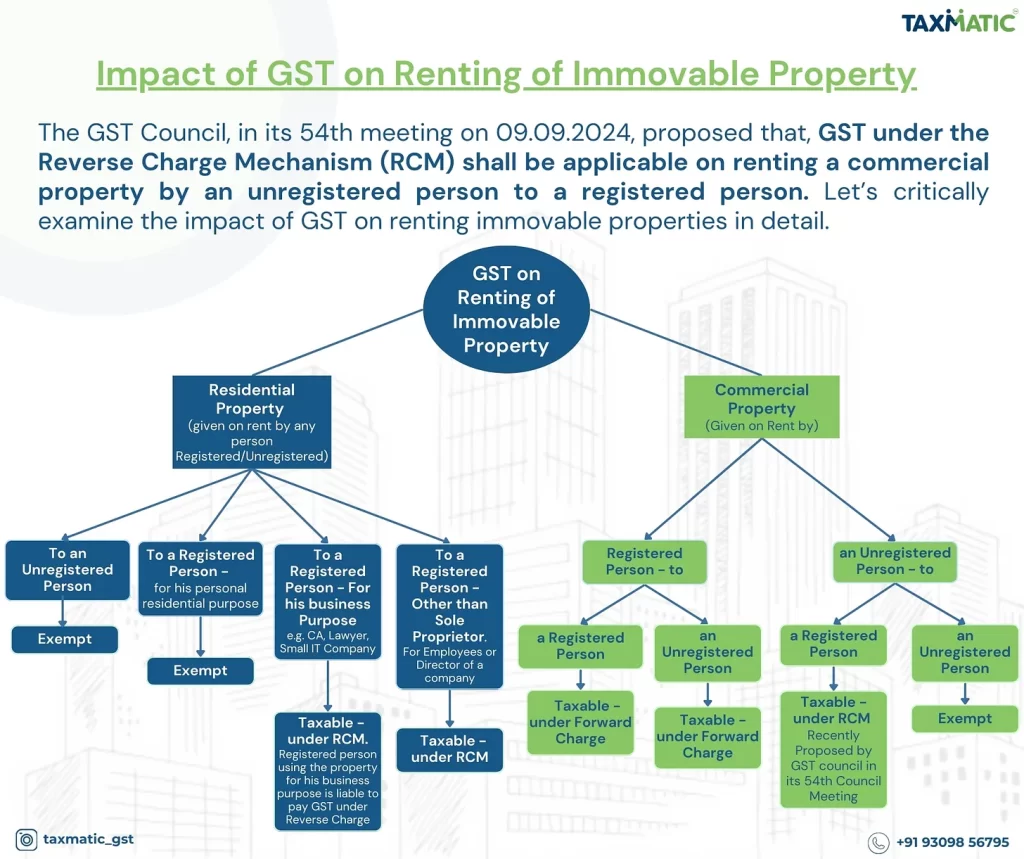

In a significant update, the GST Council, during its 54th meeting on 9th September 2024, proposed a new mechanism for applying the Goods and Services Tax (GST) to the renting of commercial properties. This change introduces the Reverse Charge Mechanism (RCM) when an unregistered person rents commercial property to a registered person.

This proposal is expected to have a notable impact on the taxation framework of commercial properties, shifting the responsibility of paying GST from the service provider to the recipient in certain transactions. Let’s dive into the key aspects of this proposal and explore how it may affect various stakeholders.

The Reverse Charge Mechanism (RCM) Explained

In the context of commercial property rentals, the GST Council has proposed that RCM should apply when an unregistered person (the landlord) rents out commercial property to a registered person (the tenant). This means that the tenant, being the registered person, will be liable to pay GST on behalf of the unregistered landlord.

The objective of this mechanism is to ensure greater compliance, simplify tax collection from unregistered persons, and streamline the overall GST system.

Key Implications of the Proposal

2. Impact on Unregistered Landlords: For landlords who are not registered under GST, this proposal may simplify their role in tax compliance, as they will not need to charge or collect GST. However, they may face indirect consequences, as registered tenants might negotiate the terms of the lease to reflect the additional tax burden they now have to bear.

3. Claiming Input Tax Credit: Registered tenants paying GST under the RCM will be eligible to claim input tax credit on the amount paid, subject to the usual conditions of the GST law. This will help mitigate the financial impact of the new tax liability on registered persons, as they can set off the GST paid against their output tax liability.

4. Greater Transparency in Taxation: This shift towards RCM for unregistered landlords is likely to enhance transparency and accountability in the GST system. It ensures that commercial property rentals do not escape the tax net due to the unregistered status of landlords, which helps in expanding the GST base.

What’s Next?

Conclusion

PS: Stay tuned for more updates as the GST Council refines this proposal. If you’re renting commercial property, it’s time to review your agreements and ensure you’re prepared for any changes ahead.